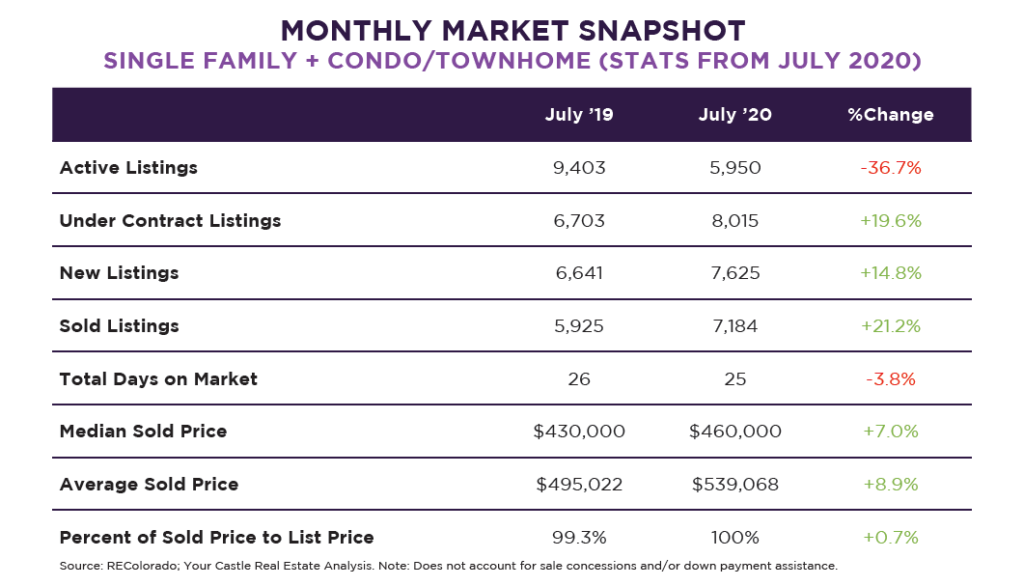

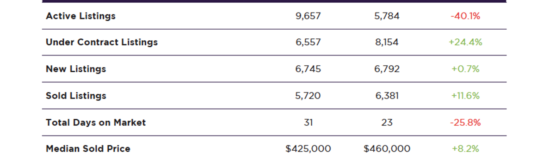

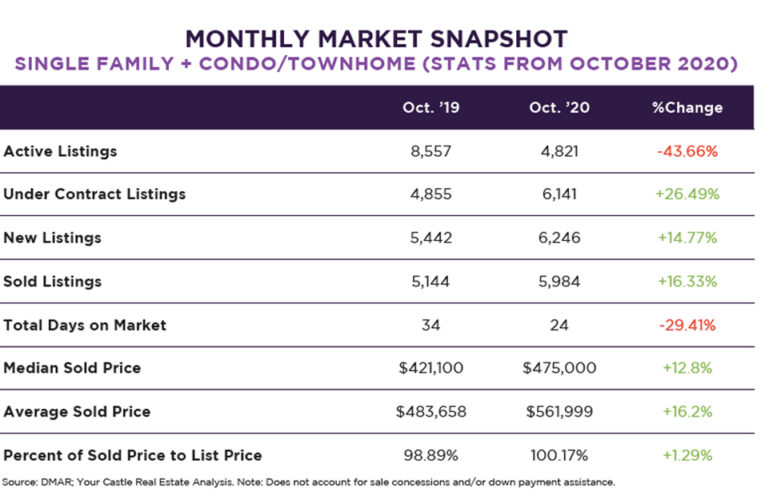

A SLOWING RECOVERY AND A RETURN TO NORMAL SEASONAL TRENDS

The speed of the real estate market recovery has finally started to slow down. In June and July, we collectively recaptured a good portion of listings not brought to the market due to the pandemic recession. Traffic reached higher levels then back in the summer of 2019 as people tried to make up for lost time in the spring. Now the numbers of newly added homes are slightly lower than this time last year. To put it more succinctly, real estate traffic now seems to be aligning with typical seasonal trends for this time of year.

However much has changed, and one of the most glaring differences is an even scarcer housing inventory. Some in the media are reporting this as an inexplicable 10% increase in the average home price in Denver since 2019, despite the pandemic and high unemployment. But that distorted average is most likely due to the mix of what is currently on the market. Since there are so few entry-level homes available, the average is being skewed closer to the higher price points. It is not that there is an excess of high-priced homes available, but rather a shortage of lower-priced homes. Do not be surprised if the media makes it seem like the sky is falling when the trend reverses – prices may “drop” in early 2021. It’s most likely not that the value of homes will be going down dramatically, it is that many sellers who opted out of selling lower-priced homes in 2020 due to financial concerns will do so next year instead. I expect that by spring of next year many of the “missing listings” will be brought to the market.

BUYERS –

EVEN TIGHTER INVENTORY AND A FLIGHT TO THE SUBURBS?

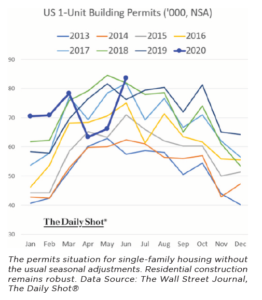

There is currently close to one month of housing inventory. This means that if no new listings were added, and the rate at which homes sell was constantly based on the average of the last 12 months of sales, it would take only one month to run out of available inventory. For comparison, during this time in 2019, the M.O.I. was closer to two months, which was also low and considered a strong sellers’ market. The demand for homes, especially entry-level homes between $0-$500K, is very high due to a housing shortage exacerbated by the pandemic. What is the bright side of all of this? Those that do secure a new home during this period are locking in record low-interest rates. This equates to a lower monthly payment. Another positive note is that building permits are up, as developers are planning to cash in on the high demand for homes. Eventually, these new permits will make up for some of the low inventory, although the process to build brand new housing can be very lengthy depending on the bureaucratic red tape in any given county. It may be more of a long-term solution than a silver bullet for the housing shortage.

Another recent phenomenon is being called a “Flight to the Suburbs” or an “Urban Exodus”. It is still too early to say if this is a long-term trend or a shorter-term effect of the pandemic, but millennials that had previously wanted to move to downtown areas for proximity to more jobs, night life, and other amenities are now buying further out in the suburbs. The current rationale is that people are working from home more than ever, so they are looking for properties with room for a home office, more living space, and a larger yard to relax in. Not to mention, they may no longer have to worry about a commute.

SELLERS –

WAITING OUT THE MARKET OR CAPITALIZING ON THE CRISIS?

Although many sellers gave up selling their homes this spring because of the pandemic, those that are selling right now are in a prime position to cash out their equity and trade up into larger homes. Between historically low-interest rates and a high demand for homes, all the drivers are in the seller’s favor. It is still a strong sellers’ market and should continue to remain so for the foreseeable future. Act now to take advantage of the current conditions before interest rates shift again.

LENDING –

MORTGAGE APPLICATIONS REMAIN AT RECORD HIGH

New mortgage applications and refinances have skyrocketed. That said, there is a reason people are scrambling to get new home loans and refinance. The interest rates are at historic lows, and as a local lender shrewdly commented, “At this point, there is more room for the rates to go up than go down.” These low rates are expected to jump up by at least half a percentage point after the presidential election, regardless of who wins, as this is the norm for any election year. If trading-up was ever a part of one’s future plans, and the finances are available, the time to do so is now – these near-zero rates will not last forever.